A couple of weeks ago I went on a bit of a rant about some terribly irresponsible reporting about how much the American Rescue Plan is spending on subsidizing private health insurance and how many people that money is expected to provide insurance premium assistance for.

The bottom line is that a whole lot of people got both the numerator and denominator wrong: Instead of being ~$53 billion to cover ~1.3 million people (which would be an insane $40,000 per person for just six months), it's actually more like ~$61 billion to help cover ~18.6 million people (roughly $3,300 per person per year on average).

On March 20th, the Vermont Health Connect ACA exchange joined other state-based exchanges in launching a formal COVID-19 Special Enrollment Period.

On April 15th, just ahead of the original SEP deadline, they bumped it out by a month.

Then, with the May deadline approaching, I took a look and sure enough, they've bumped it out another month.

And now, with the June deadline having come and gone...

Due to the COVID-19 emergency, Vermont Health Connect has opened a Special Enrollment Period until August 14, 2020.

I admit that this is starting to get a bit silly. At a certain point I'm guessing at least one of the state exchanges will just say "screw it" and open 2020 enrollment up for the full year.

When the $1.9 trillion American Rescue Plan (ARP) achieved final passage on March 10th, it did so almost exclusively along party lines. I say "almost" because there was a single Democratic House member who voted against it: Representative Jared Golden (ME-02).

I fully understand the tightrope that some swing district Dems have to walk. To his credit, Rep. Golden voted to impeach Donald Trump not once, but twice (though he only voted in favor of one of the 2 articles of impeachment against him the first time around). I certainly don't expect every single Democrat to vote the party line on every single bill.

In the end, the bill passed anyway, if only by a handful of votes; my guess is that he even received Speaker Pelosi's unofficial blessing to vote against it, as long as she knew for sure it would pass regardless.

Everyone who spread this disinformation was getting both the numerator and the denominator wrong. In short, they were claiming that the federal government was going to spend up to $53 billion to provide healthcare coverage to a mere 1.3 million people for as little as a six-month period (which would amount to an insane $80,000 per year apiece if true...which it isn't).

As I explained in painstaking detail, the actual amount being spent per person is more like $3,300 apiece for anywhere from 14.2 million to 18.6 million people depending on whether you're going by the House or Senate CBO score (and the final version of the ARP was the Senate version).

NOTE: SEE SUMMARY TABLE IN UPDATE ALL THE WAY AT THE END.

I'm doing my best to stop myself from putting my head through a wall this weekend.

You may have seen this viral tweet making the rounds over the past day or so:

The Democrats just spent $52 billion to subsidize COBRA for 1.3 million people until September. That’s $40k per person for less than 6 months of health insurance. Most countries spend about $5-6k per person per year for universal healthcare.

This was posted at 12:22pm on Friday, March 12th, 2021. It's still live as of 11:00am on Sunday the 14th, has over 32,700 Likes and has been retweeted over 7,300 times as of this writing, but in case it's deleted by the time you read this, here's a screen shot:

It's important to note that the following guidelines only apply to residents of the 36 states hosted via HC.gov. The timing, policy and procedures for the new/expanded subsidies for residents of the 15 states which operate their own ACA exchanges may vary.

The short version is that because his income is so low, he normally wouldn't be eligible for ACA subsidies...except because he lives in Maryland, a Medicaid expansion state, he would normally be eligible for Medicaid...except that because he's an immigrant who's been in the United States for less than five years, he isn't eligible for Medicaid...except that, thanks to an obscure provision baked into the Affordable Care Act, he is eligible for ACA subsidies after all!

‘(B) SPECIAL RULE FOR CERTAIN INDIVIDUALS LAWFULLY PRESENT IN THE UNITED STATES.—If—

‘‘(i) a taxpayer has a household income which is not greater than 100 percent of an amount equal to the poverty line for a family of the size involved, and

During the early days of the Affordable Care Act (and again during the insane "Repeal/Replace" saga of 2017), one of the dumbest and most disingenuous talking points of Republicans was to attack the ACA for being "too long."

I'm quite serious...many Very Serious Conservatives stroked their beards and wrung their hands over the sheer length of the ACA's legislative text (officially around 2,700 pages, though if you includ the mountain of regulations which are included with any major bill impacting hundreds of millions of people it could theoretically be tracked at 20,000 pages or so).

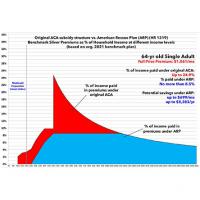

In early February, I posted a deep dive into HR 369, the Health Care Affordability Act, and how it would reduce net ACA premiums by permanently eliminating the income "subsidy eligibility cliff" (#KillTheCliff) and making the underlying subsidy formula more generous for all enrollees (#UpTheSubs).

I'm re-posting an updated, modified version of this analysis for two reasons:

First, because HR 1319, the American Rescue Plan, is about to actually pass and be signed into law, with a slightly different formula from HR 369 embedded within it (if only for two years).

Second, because my earlier analysis also threw in two other subsidy enhancement tables which confused the issue (California's state-based subsidies, and the predecessor to HR 369, both of which are/were less generous)

In this version I'm using the actual Advanced Premium Tax Credit (APTC) table under the American Rescue Plan, and I'm cutting out all references to the other two tables to avoid confusion.

Nearly every state (+DC) has re-opened enrollment on their respective ACA exchanges in response to both the ongoing COVID-19 pandemic and the American Rescue Plan (ARP), which substantially expands and enhances premium subsidies to millions of people!

If you've never enrolled in an ACA healthcare policy before, or if you looked into it years ago but weren't impressed, please give it another shot now. Thanks to the ARP (and some other reasons), it's a whole different ballgame this spring & summer.

Here's 10 important things to understand when you #GetCovered: