Connect for Health Colorado, the state's ACA exchange, has published effectuated enrollment data for January, February and March 2026, so it's time to dig in and see what this might say about national trends.

Unfortunately, it doesn't provide much demographic data (metal levels, income levels, etc), but it does at least provide the number of effectuated enrollees as well as new and terminated enrollments.

Below is what it looks like compared to the same months in prior years. I'm disregarding the COVID years (2020 - 2023) but am including 2016 - 2019 (none of which included the enhanced federal tax credits) as well as 2024 & 2025.

Officially, Qualified Health Plan (QHP) selections during Open Enrollment were only 1.9% lower than they were in 2025. However, as I expected and have warned about repeatedly, the year over year drop in effectuated enrollment was double that in January (3.8%), and the gap grew in both February and March. For the first quarter of 2026, effectuated enrollment in Colorado is down 5.3% vs Q1 2025.

Finally, there's nearly 1.1 million exchange enrollees who earn more than 400% FPL...although this total is actually closer to 2.15 million if you include enrollees whose household income is either "other" or "unknown:"

The application only collects household income data when consumers are requesting financial assistance.

Consumers that do not request financial assistance do not enter their household income information and are classified as having an “Other/Unknown FPL.”

There are a few SBEs that classify consumers who enter their household income information but are determined not eligible for financial assistance as “Other/Unknown FPL”. As a result, some SBEs report zero plan selections in certain income categories. Please refer to the Public Use Files Definitions document for additional information on these data.

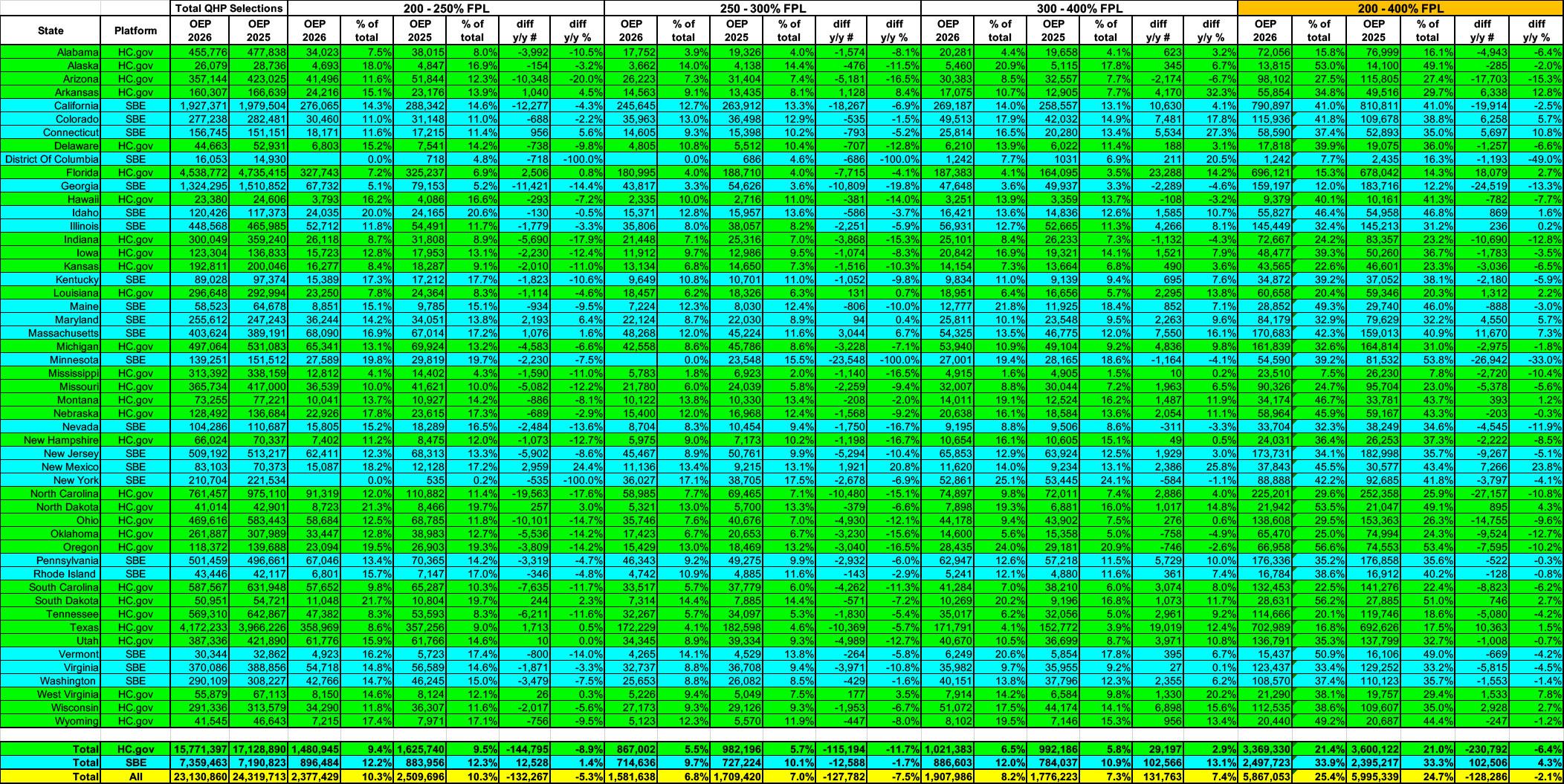

Next, let's look at the 200-400% FPL bracket. These make up just over 1/4th (25%) of total ACA exchange enrollment this year, up slightly from last year.

Overall enrollment in this bracket only dropped by about 2.1% (128,000 people), which makes sense for several reasons:

First, they were the least-impacted by the enhanced subsidies expiring (most of them still saw their premiums jump dramatically, just not as dramatically as those below 200% FPL or over 400% FPL)

Second, the Trump Regime policy change making recent (under 5 years) documented immigrant residents ineligible for federal tax credits doesn't really apply to this population anyway.

However, there's a third reason for the relatively small drop-off in this income range which I'll address below....

Through the new program, Get Covered Illinois connects uninsured Illinois tax filers and their families to quality, affordable health coverage.

CHICAGO — Open enrollment has ended, but uninsured Illinoisans can still enroll in a health insurance plan through the state’s new Tax Time Easy Enrollment program. The program provides a pathway to coverage for residents as part of the annual tax filing process. With the deadline to file taxes approaching on April 15, Get Covered Illinois is encouraging filers to take advantage of this new program.

Turning to the 100 - 200% FPL range, 64% of all exchange enrollees fall into this income range (up slightly from 63% last year).

That's ~14.8 million people total, with ~10.7 million earning 100 - 150% FPL and the remaining ~4.1 million earning 150 - 200% FPL.

The vast majority of those in the first bracket (and most of those in the second) should be enrolled in Silver plans since they're eligible for generous CSR assistance which boosts Silver plans up to "Secret Platinum" status: If they earn up to 150% FPL Silver plans have a 94% Actuarial Value; if they earn 150 - 200% FPL Silver is boosted to 87% AV.

In layman's terms, High CSR Silver plans have either free or extremely low premiums along with extremely low deductibles & co-pays.

This is, of course, extremely important since household income is one of the most critical factors in calculating how much financial assistance enrollees receive (or if they're eligible for Advance Premium Tax Credits (ATPC) at all).

Since there's so many income bracket columns and there's a lot to delve into for many of them, I've broken the full spreadsheet out into several sections/posts. The first focuses on exchange enrollees who earn less than 138% of the Federal Poverty Level (FPL). This is a critical threshold because it's the cut-off point for ACA Medicaid expansion eligibility in the 40 states (+DC) which have expanded the program.

There's actually two distinct populations here: Enrollees who earn less than 100% FPL and those who earn between 100 - 138% FPL.

Note: This section is so chock full of tables & graphs that I've broken it into two sub-sections...I'll be posting the 2nd half of Part 5 over the weekend...

If you've ever wondered why healthcare wonks (myself included) rarely talk about the ACA's Catastrophic Level plans (or at least it was rare up until last year, when the Trump Regime decided to try opening up the floodgates on them), and why the only time I usually discuss Platinum Plans is in the context of high-CSR enrollees being eligible for "Secret Platinum" plans (labeled as Silver), the first table below should explain why.

Catastrophic ACA plans are only available at all in 34 states +DC (this is actually down from 40 states +DC last year), and less than 0.3% of all ACA exchange enrollees choose Catastrophic plans...just 67,000 nationally. Even if you only include the states where they're available this only increases to 0.36% (although they did reach 4.4% of total enrollments in Montana this year).

Note: This is mostly an updated version of a post of mine from last May, when it looked as though Senate Republicans were going to include "funding CSR reimbursement payments" as part of their Big Ugly Bill (officially the "One Big Beautiful Bill Act") which, among many other terrible things, included gutting Medicaid and didn't include extending the ACA's enhanced premium tax credits beyond December 2025.

Thankfully, in the end the Senate GOP didn't include the CSR funding provision...but House Republicans did include it in a bill which they passed last winter...which then died in the Senate since it would have required 60 votes there to move forward.