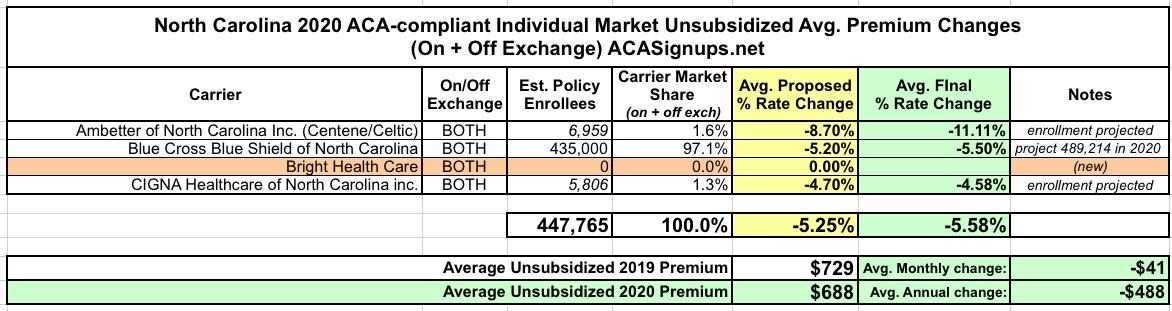

North Carolina has three individual market carriers in 2019. For 2020, that's increasing to four, as Bright Health Care is expanding into the NC market. The other three carriers (Blue Cross Blue Shield has a near monopoly at the moment) had requested average unsubsidized rate drops of 5.3% previously; in the end the final rates are dropping slightly more, to -5.6%.

Cigna extended its individual healthcare exchange products for the 2020 plan year, the insurer said Sept. 18.

For 2020, individuals can purchase individual health plans in 19 markets across 10 states. The expansions will take place in counties in Kansas, South Florida, Utah, Tennessee and Virginia. The other states include Arizona, Colorado, Illinois and North Carolina.

The plans will be available for purchase on the individual marketplace during the 2020 open enrollment period, which begins Nov. 1. Plans will take effect Jan. 1.

But that's not all! In addition to the actual 2018 MLR rebates, I've gone one step further and have taken an early crack at trying to figure out what 2019 MLR rebates might end up looking like next year (for the Individual Market only). In order to do this, I had to make several very large assumptions:

NOTE: This post re. North Carolina's 2020 individual market premium rate change is incomplete because it only includes one of the three carriers participating in NC's market (Blue Cross Blue Shield of NC). The rate change requests for Cigna and Centene haven't been released yet.

Normally I'd wait until I had data for the other two as well, but BCBSNC held around 95% of the state's Individual Market share last year, with Cigna holding the other 5% (Centene was a new entry to the market, so they didn't have any of it). I don't know how much the relative share has changed this year, but I'm assuming that BCBSNC still holds the lion's share of the total.

Blue Cross NC is decreasing 2020 Affordable Care Act (ACA) rates by an average of 5.2 percent for plans offered to individuals and an average of 3.3 percent for plans offered to small businesses with one to 50 employees. With this reduction, we take 238 million steps towards more affordable care in North Carolina.

Senate OKs small business health-care bill

By Richard Craver Winston-Salem Journal

The state Senate gave initial approval Wednesday to a Senate bill that would allow small-business employers to offer an association health-insurance plan, or AHP, that could provide lower premium costs.

Senate Bill 86 received a 40-8 vote on second reading, but an objection to a third reading kept it on the Senate calendar until at least today.

The GOP holds a majority in the NC Senate, but only by 29 to 21, so stopping this there was apparently a lost cause. They also hold a 65 to 54 majority in the state House. I'm not sure whether SB 86 has already been voted on there or not. If it passes both, it would be up to Democratic Governor Roy Cooper to veto the bill.

North Carolina has three insurance carriers offering individual market policies next year: Blue Cross Blue Shield, which holds a whopping 96% of the individual market; Cigna, which holds the remaining 4%, and newcomer Ambetter (aka Centene).

BLUE CROSS NC FILES TO LOWER ACA RATES BY AVERAGE OF 4.1 PERCENT

Durham, N.C. – Blue Cross and Blue Shield of North Carolina (Blue Cross NC) announced today it requested an overall average rate decrease of 4.1 percent for 2019 Affordable Care Act (ACA) plans offered to individuals. The reduction marks the first rate decrease in the history of Blue Cross NC since entering the current individual market more than 25 years ago.

...Many factors went into the Blue Cross NC’s rate filing:

There are only two insurance carriers participating in the North Carolina individual market this year: Blue Cross Blue Shield and Cigna. That's expected to change for 2019, as Centene (aka Ambetter) is expected to jump into the NC market, but in terms of premium changes, it's just BCBS and Cigna which can be counted in my 2019 Rate Hike project.

One of the big stories over the past few months has been the Trump Administration's attempts to strip away regulations on non-ACA compliant "Short-Term, Limited Duration" plans (by making them neither short-term nor of limited duration) and "Association Health Plans" (by recategorizing them from state-regulated, Small Group plans to mostly unregulated Large Group plans).

The Iowa Senate voted Wednesday to let the Iowa Farm Bureau Federation and Wellmark Blue Cross & Blue Shield sell health insurance plans that don't comply with the federal Affordable Care Act.

The new coverage could offer relatively low premiums for young and healthy consumers, but people with pre-existing health problems could once again be charged more or denied coverage.

As I noted last week, insurance carriers in North Carolina were supposed to have submitted their preliminary 2019 premium rate change filings as of May 21st. Unfortunately, as I also noted last week, those "deadlines" appear to be more "guidelines" in many states, with North Carolina among them; there's no publicly-available premium change data available yet.

Insurers that wish to offer individual market coverage in North Carolina in 2019 had to file rates and forms by May 21, 2018. The two insurers that offer 2018 coverage in the North Carolina exchange — Cigna and Blue Cross Blue Shield of North Carolina — have both filed rate for 2019. Although the filings do show up in SERFF, they have very little publically available data at this point.

Way back in May, Blue Cross Blue Shield of North Carolina submitted their initial 2018 rate requests to the state insurance department, and noted at the time that they'd normally only be requesting an 8.8% average rate increase...but that due specifically to Donald Trump's threat to cut off CSR reimbursement payments, they were asking for a 23.3% increase instead. I noted that this meant that about 60% of their increase request was caused by Trump's CSR threat.

Then, in August, they gave a somewhat more positive news update: They were lowering their requested rate hike to 14.1%. Basically, their latest numbers had come in and the balance sheet was doing quite a bit better than they had previously thought:

Blue Cross said May 25 that the 22.9 percent rate increase was based on the subsidies ending, along with claims data from the first quarter of 2017. It projected an 8.8 percent rate increase with the subsidies remaining in place.