As I noted a month ago, Virginia insurance carriers participating in the ACA individual market submitted preliminary 2024 rate filings which averaged over a 20% hike, almost entirely due to the prospect of the states reinsurance program (which had only been implemented one year earlier) possibly not being funded for the second year.

In 2023, average unsubsidized indy market premiums in Virginia had dropped by around 13% thanks to the new reinsurance program, which offloads a portion of high-cost enrollee care to the federal government in return for reducing the amount of subsidies received by low/moderate-income enrollees.

Fortunately, cooler heads eventually prevailed, and in the end the state legislature passed a budget which did indeed properly fund the program. This allowed insurance carriers to file modified rates for 2024 which include the reinsurance program being in place.

Maryland Insurance Administration Approves 2024 Affordable Care Act Premium Rates

Reinsurance Program Continues Positive Impact on Individual Rates

BALTIMORE – Maryland Insurance Commissioner Kathleen A. Birrane today announced the premium rates approved by the Maryland Insurance Administration for individual and small group health insurance plans offered in the state for coverage beginning Jan. 1, 2024.

Rate Changes for the Individual Market

The rates for individual health insurance plans subject to the Affordable Care Act (ACA) will change/increase by an average of 4.7% for 2024. Approximately 229,000 Marylanders are impacted by the approved rates. However, the actual percentage by which the rates for a specific plan will change depends on the carrier and plan.

Arkansas is a problematic state for many reasons, but I have to give their insurance dept. website high praise for posting their annual rate filings in a clear, simple & comprehensive fashion (which is to say, not only do they post the avg. premium changes for each carrier, they also post the number of covered lives for each, which is often difficult for me to dig up). Better yet, they also include direct links to the filing summaries and include the SERFF tracking number for each in case I need to look up more detailed info.

Anyway, there's nothing terribly noteworthy in the 2024 filings. Insurance carriers sought an average 5.0% rate hike on the individual market and 5.5% for small group plans; these were shaved down slightly by state regulators for overall weighted average increases of 4.1% and 5.4% respectively.

USAble HMO is launching a new line of HMO insurance products in the state next year (called "Octave" I believe) but otherwise it looks pretty calm.

CONNECTICUT INSURANCE COMMISSIONER ANNOUNCES 2024 HEALTH INSURANCE RATES SAVING ACA HEALTH INSURANCE PLAN MEMBERS $96.2 MILLION AND HOLDING INSURER PROFITS TO 0.75%

(Hartford, CT) – In a significant move to protect Connecticut consumers against unsupported health insurance cost increases, Connecticut Insurance Commissioner Andrew N. Mais announced today that the Connecticut Insurance Department (CID) continues to protect consumers by reducing health insurers’ 2024 requested rates, despite ongoing increases in underlying health care costs. These 2024 rates are for individual and small group plans offered on and off the state exchange Access Health CT. The Connecticut Insurance Department does not regulate self-funded plans which fall under the authority of the U.S. Department of Labor.

A few weeks ago, I noted that Virginia's average 2023 unsubsidized ACA individual market premiums dropped by nearly 13% thanks to the newly-implemented state-based reinsurance program...but that they were at risk of skyrocketing by as much as 25% in 2024 due to that same reinsurance program being at risk of not continuing for a second year because of a budget standoff:

During 2021, the Virginia General Assembly passed HB 2332, the Commonwealth Health Reinsurance Program, which was signed into law on March 31, 2021 as Chapter 480, of the 2021 Virginia Acts of Assembly. This bill requires the State Corporation Commission to submit a waiver request for federal approval to establish a reinsurance program beginning January 1, 2023.

Massachusetts, which is arguably the original birthplace of the ACA depending on your point of view (the general "3-legged stool" structure originated here, but the ACA itself also has a lot of other provisions which are quite different), has 10 different carriers participating in the individual market.

One thing which sets Massachusetts (along with Vermont) apart from every other state is that their Individual and Small Group risk pools are merged for premium setting purposes.

Normally you would think this would make my job easier, since I only have to run one set of analysis instead of two...but until recently, it was surprisingly difficult to get ahold of exact enrollment data for each carrier on the merged Massachusetts market (and even more difficult to break out how many are enrolled in each market since they're merged...not that that's relevant to the actual rate changes).

Salem – Oregon consumers can get a first look at requested rates for 2024 individual and small group health insurance plans, the Oregon Department of Consumer and Business Services (DCBS) announced today.

In the individual market, six companies submitted rate change requests ranging from an average 3.5 percent to 8.5 percent increase, for a weighted average increase of 6.2 percent. That average increase is slightly lower than last year's requested weighted average increase of 6.7 percent.

In the small group market, eight companies submitted rate change requests ranging from an average 0.8 percent to 12.4 percentincrease, for a weighted average increase of 8.1 percent, which is higher than last year's requested 6.9 percent average increase.

Tennessee's preliminary 2024 individual & small group market health insurance rate filings are now available, including actual enrollment numbers, which allows me to run weighted averages for both markets.

For the most part they're fairly straightforward: The individual market is looking at average rate increases of around 4.8%, while the small group market averages around +7.8% overall.

UPDATE 10/02/23: Well, all of Tennessee's filings appear to have been approved as is by the state regulatory department...they all say "approved" at the SERFF database and the newest filing versions all predate the original publication of this blog post from 8/17, so I'm concluding the preliminary rates are also the final rates.

Back in June, the New York Department of Financial Services published the preliminary annual rate filings for both the individual and small group health insurance markets. At the time, the NY DFS put the weighted average rate increases on the ACA-compliant individual market at 20.9% statewide, although my own calculations based on the officially-reported market share enrollment came in slightly lower, at 20.7%.

Meanwhile, they put small group market, NY DFS put it at a 15.3% average increase (almost identical to my 15.4%).

However, I made sure to include an important caveat:

It's important to remember that these are not final rate increases--New York in particular has a tendency to slash the requested rate hikes down significantly before approving them.

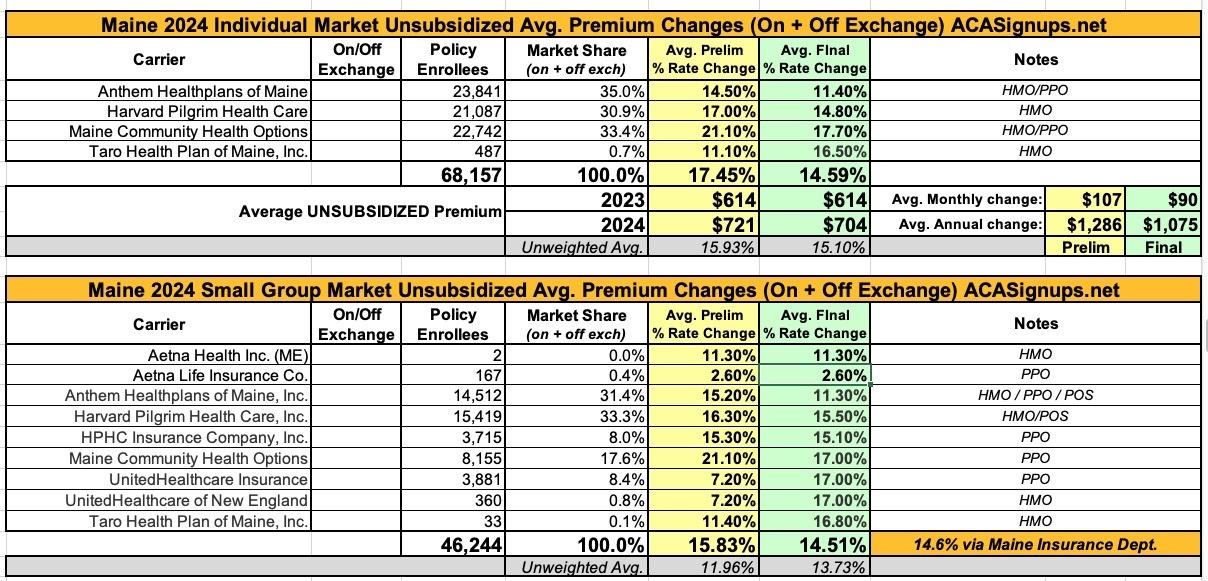

At the time, the weighted average rate increases requested by insurance carriers in Maine were a steep 17.9% hike for the individual market and a 15.8% increase on the small group market.